Loss of Earnings with 7 days deductible is back!

Loss of Earnings with 7 days deductible is back!

14/90/90 at 2.00% or 7/97/97 at 2.40% ... Should that be a question?

Let me expand on the background that has led to the somewhat provocative question I am asking.

For the last 25-30 years, ship owners have been buying conventional LoH on terms like 14/90/90, 14/180/180 or other variations of it but with the constant common feature that they must always retain the first 14 days cash flow exposure of a H&M casualty.

WHY ?

One of the answers is probably that for the last 25 to 30 years this has been the only available option to a shipowner, except for the domestic Japanese market.

Before that, conventional LoH was available in the marine insurance market worldwide with a lower deductible, usually 7 days, but underwriters stopped writing it after the losses in the 7 to 14 days’ layer of a casualty got too high and business became unsustainable.

With no longer that option available many first class owners were forced to switch to full self-insurance for the first 14 days.

This, amongst other factors, was the drive when we started up Nordic Marine. Our aim was, and remains, to be the reference player that can fill the gaps in the mainstream insurances like LoH, H&M or P&I.

Our Delay cover provides ship owners with a way to protect the first 14 days’ cash flow after a ship or shore incident delays the vessel. It is a tailor made insurance, quoted and adapted around the individual needs of a shipowner, and our Delay portfolio currently protects over 1,200 ships.

During our first, successful, 10 years we developed an ever-closer relationship with clients and brokers. We collected their feedback and we recently acted on their requests for a mainstream-like cash flow protection insurance that would respond in the same layer as the Delay cover but have the same mechanics as the mainstream LoH.

"Both clients and brokers called for an alternative solution that did not need a “tailors’ hand”."

It is for that reason that Nordic developed the Primary Loss of Earning (PLoE) insurance, a semi mainstream insurance that protects a ship owner’s cash flow during the first 14 days following a H&M incident.

Our PLoE cover is triggered by the main H&M policy, as is conventional Loss of Hire, and the differences with conventional Loss of Hire are the following :

Delays following damages discovered during drydocking are excluded.

Delays commencing more than 90 days after the first occurrence or commencement of the event are excluded, unless previously agreed otherwise in writing by underwriters.

No Reinstatement premium in case of claim, i.e.: cover is automatically reinstated at no extra cost, always subject to policy annual aggregate limit over all declared ships.

After this short review of conventional LoH and Nordic’s Primary Loss of Earning, I will go back to the question I started with.

"Why does a shipowner retain the highest risk of 14 days when there is now an option to buy an insurance for it?"

The most common answer is that it is too expensive or yet another cost for a ship owner, and in this article I have decided to challenge the ratio leading many players to have this perception.

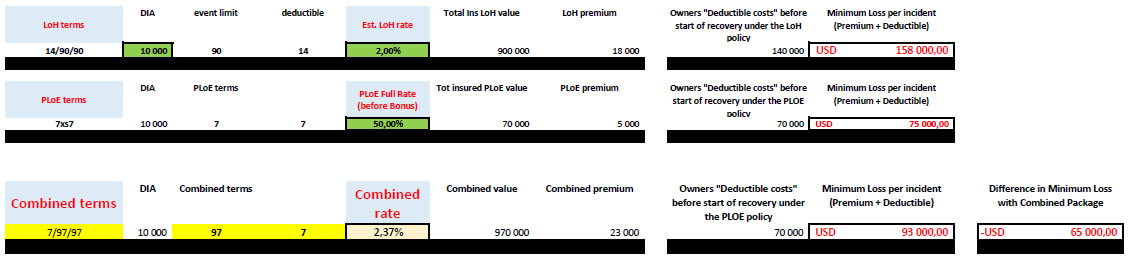

If we look at the most common LoH package, 14/90/90, the average rate for a ship owner with decent records will be around 2%, so with a declared daily insured amount of 10 000 USD the annual premium for one vessel will be USD 900 000* 2%, i.e. USD 18 000.

OR WILL IT ?

The answer is no, the real costs for an Owner who has a claim for loss of earning during a delay of say 30 days will be the USD18,000 due to the LoH insurers, plus the deductible of 14 days * USD10,000, i.e.: USD158,000. On top of that we normally have the reinstatement premium, but will leave that one outside the calculation since it depends on the number of used LoH days.

The mathematics are easy!

The actual cost

So, USD158,000 is the true cost that an owner will have to swallow before they start recovering from their conventional LoH policy, if of course their daily earning are of USD10,000, but recent freight market rates can dwarf that level.

It is almost as if the focus of an owner when they consider buying conventional LoH as cash flow protection is on when recovery starts, which in our view is not the best approach.

In fact, what good is it to know when you start recovering, if by then, you have already lost a fortune?

Would it not be a (much) better approach to – first – focus on when can I, as ship owner, stop losing money after a casualty occurs?

The answer is very simple: the sooner the better!

Yes, but you might say that buying more cover means more costs, right?

Of course the answer to that is yes, but (unsurprisingly, you might say) I don’t think it is the right question. The right question when you want to transfer the burden for the highest risk is whether that transfer will cost you more than the burden you know you will face.

Let’s look at the mathematics of buying a combined PLoE and LoH insurance cover that would enable a ship owner to stop the losses after only 7 days.

If we use the same example as above and add the PLoE rate that Nordic would probably apply given the same ship owner profile, you will get the following picture:

What does the above mean ?

It means that, potentially, by paying an additional premium of USD 5 000, i.e.: USD23,000 instead of USD18,000, a ship owner can reduce the cash flow exposure following a H&M incident from USD 158,000 down to USD 93,000, NB: including the “additional” insurance costs.

The cash flow exposure during the first 14 days is, by far, the highest risk period, as any superintendent could confirm and as conventional LoH underwriters infer through not offering LoH cover with 7 days deductible.

The above is, I would say, a very strong challenge to the argument that buying Primary Loss of Earnings is an additional expense for a ship owner. Rather, it seems clear to me that the above example shows that in case of a H&M incident the Owner’s total costs will actually be reduced.

And, just in case you think such incidents do not happen to you, bear in mind that in the past 10 years, our underwriters have analyzed the H&M statistics of well over 1,000 shipowners in the process of assessing their risk profile and if possible propose terms.

Without a doubt, most of the shipowners have had claims that delayed the vessel in excess of a few days but often below 14 days.

At the end of the day, and statistics aside, basic common sense tells, clearly, where owners’ immediate and unavoidable financial losses occur.

Our underwriting process

Our underwriting process delivers a sustainable quasi-mainstream solution for the highest risk exposure, so I am always surprised to hear that there are owners for whom reducing their primary cash flow exposure from USD 140 000 to 70,000 USD at a cost of around 5,000 USD is still a question.

A cover that can be taken with or without conventional LoH cover being in place.

A cover that Nordic is the only insurer to provide, thanks to the exceptional underwriting performance, track record and professional diversity of the UW team’s profile.

As many of you know, I am a P&I claims veteran, Claudio Blancardi a reference for Delay insurance and a remarkable Hull Team headed by Jan Limnell, a reference in global markets, and including known professionals like Constantinos Elmaoglou, Yiannis Minovioudis and Mathias Lindqvist.